What do successful mobile gaming companies do differently? How do the best mobile game apps win? How are mobile game developers attacking the iOS and Android segments of the mobile gaming market differently? And what kind of ROI and ROAS are the top mobile games making?

It’s been a while since I’ve taken a deep dive into mobile gaming installs, revenue, and ROI numbers, and frankly, it’s about time.

The mobile advertising market is in upheaval thanks to SKAdNetwork, mobile adtech companies are buying each other left, right, and center, what we think we know about mobile advertising on iOS and Android is changing rapidly, and game developers and marketers still need to operate and advertise in an increasingly complex growth data environment.

We took this opportunity to look at 20 of the world’s top gaming companies and analyze what they’re doing to succeed in the changing mobile marketing ecosystem.

A few of the highlights upfront

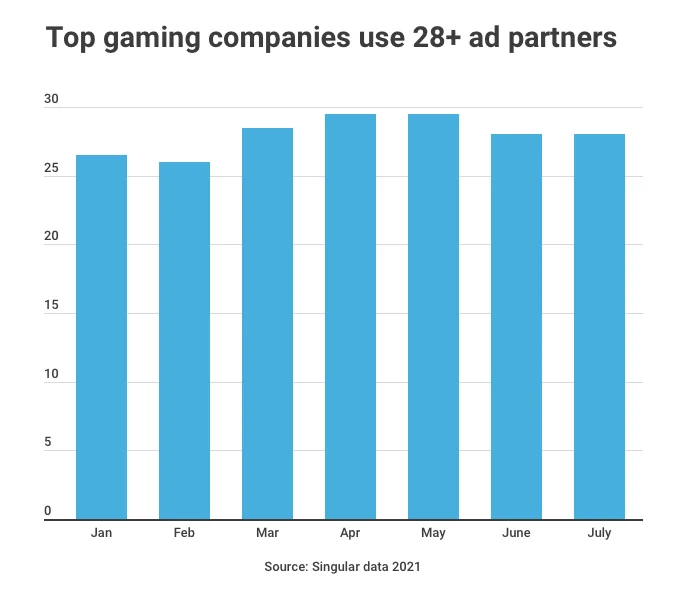

- Top gaming companies use 2-3X more ad partners than average mobile app marketers

- 8 out of every 10 mobile gaming app install are on Android

- But only $5-6 out of every $10 spent on mobile app installs is spent on Android

- SKAdNetwork is normalizing ad spent between Android and iOS

- ROI looks higher on iOS when organic revenue is included

- ROI is higher on Android when organic revenue is excluded

Mobile gaming advertisers use a LOT of partners

While there are outliers, small-scale mobile advertisers who are less successful tend to use just a few ad partners. In the past I’ve seen groupings around four — usually a group of SANs including Facebook and Google — and significant jumps in performance for marketers with massive scale at over ten.

Mobile games advertisers knock that out of the park.

The median number of ad partners per month varies, but for the most successful gaming companies, it’s generally in the high twenties. There are outliers, of course. The lowest we saw was 10, while the highest number of ad partners with active campaigns in a single month for a top gaming publisher was 60.

That’s impressive, but it’s not the highest I’ve ever seen. It’s not unheard of for top game advertisers to have over 100 active partners in a given month.

More partners mean more management, of course, so all other factors being equal, the fewest number of partners you can successfully grow with is good. But most top mobile game marketers find they can access efficient growth opportunities better with a fairly high number of ad partners.

Advertisers should look for programmatic partners who can help them carve this path, who are prepared and understand how old strategies can be revamped to this new industry reality, and who are 100% transparent at every level.

A programmatic DSP (Demand Side Platform) provides advertisers access to incremental uplift enabling advertisers to understand how much value a channel is adding to their advertising. This way, your decisions to optimize your campaigns are backed by data and ROI-focused.

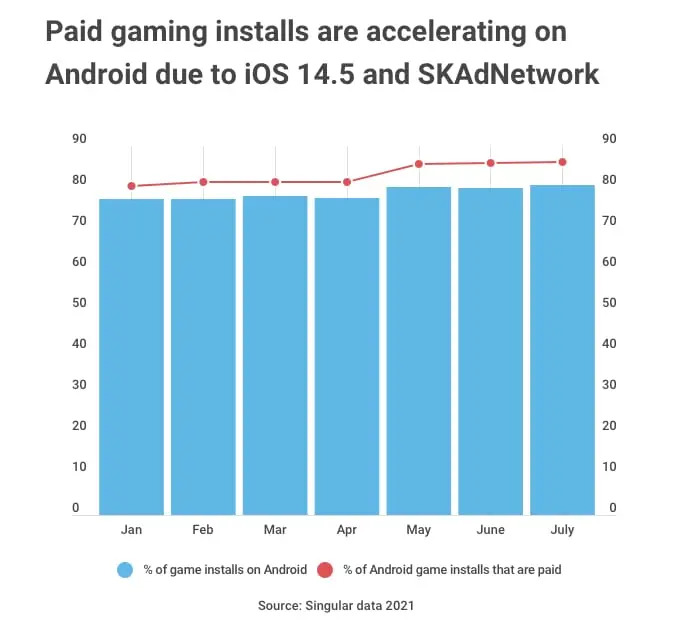

SKAdNetwork is increasing Android’s share of game installs

Everyone knows that Android has significantly more market share than iOS. While in the U.S. that’s simply a 54% to 47% edge (rounded, so numbers can total more than 100%), China is 82% Android, Brazil is 94% Android, and even the richer European countries tend to be 60-80% Android.

So it’s no real shock that eight out of every 10 game installs are on an Android device.

But it is interesting that that percentage is growing, and that it’s driven by increasing spend on Android marketing campaigns.

At the beginning of 2021, 77 out of every 100 game installs for top mobile game publishers were on Android. In the last three months, that’s edged up to 80 out of a hundred. Note: The overall number of app installs for Android games is not significantly up (keep reading!) but the percentage of all games installed on mobile (iOS + Android) is. This means, of course, fewer games are getting installed on iOS.

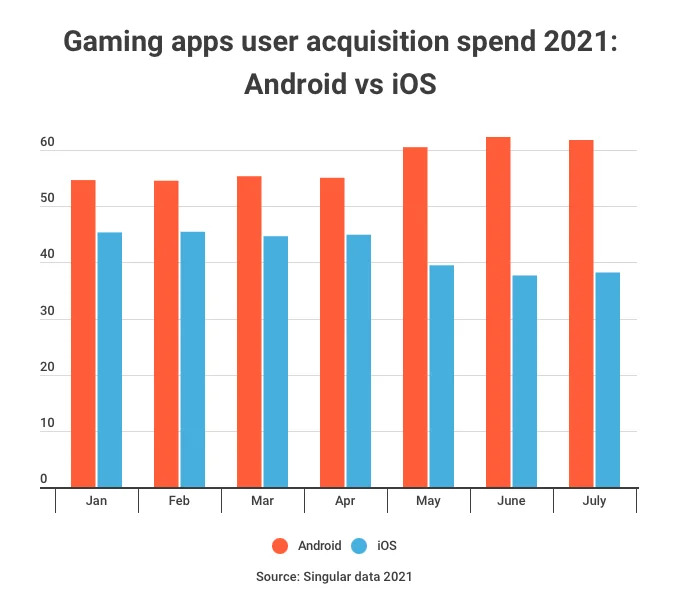

Driving that is significant amounts of paid app install spending moving from iOS to Android, and that’s driven a rise in the percentage of game installs on Android that are paid increasing to 86% from previous levels of around 80%.

While at the beginning of the year 54-55% of gaming publishers’ ad spend was focused on Android, now 60% or more is directed to Android app installs versus just 40% or less for iOS. (Note: the July data is limited, so I’m basing my analysis on the April/June data. But so far, the July data appears to be fully on-trend.)

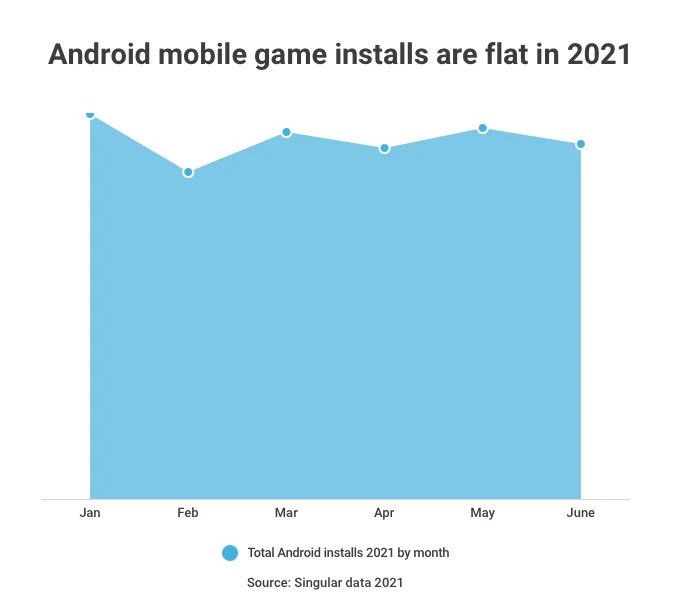

Unfortunately, that spending does not appear to be increasing the overall installs of games on Android. In fact, total game installs on Android are essentially flat across 2021.

Which means that so far, we have the worst of all possible worlds.

Ad spend is down on iOS because measurability by traditional mobile user acquisition methods using IDFAs is gone. That ad spend has transitioned to Android because … growth targets must be met. But instead of generating new demand on Android, the new ad spend is simply taking a share of installs that would otherwise have happened in any case via organic.

Of course, when looking at big trends you need to compare them to previous years to see if what you’re seeing is a seasonal event or a real consequence of some major industry change. As I reported in a somewhat aged holiday trends report:

Big picture, the app install cycle is simple: slow in February/March/April, ramping in late spring and early summer, and peaking in October, November, and December, with some run-off into January.

This is significant: the ramping that we should be seeing in the spring and early summer numbers is conspicuously absent.

The caveat of course is 2020. We just came out of a crazy year. We’re in the middle of another crazy year, with COVID and its aftermath (can we say that yet?) still wreaking havoc on people, economies, and natural cycles of activity, shopping, pricing, and more. So take that insight with a grain of salt … but it seems, so far, to be valid.

All of which means … we should take a hard, skeptical look at ROI and ROAS

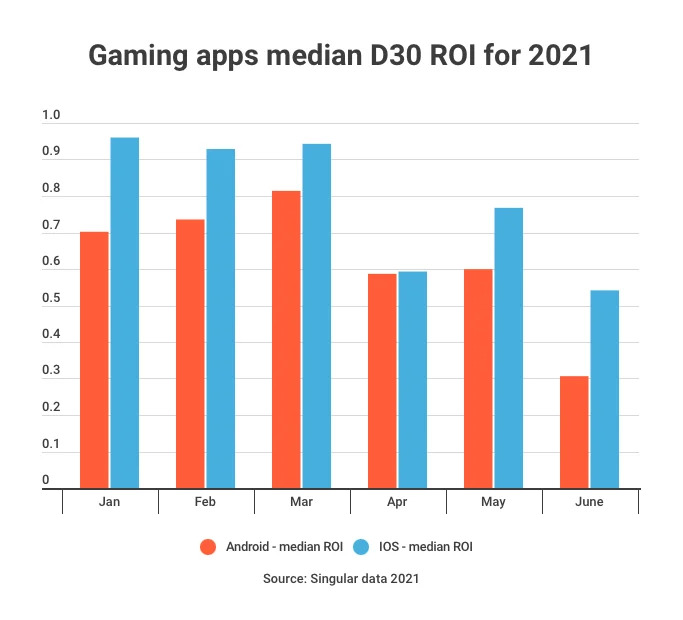

In crazy, turbulent times, it’s worth looking at whether ROI and ROAS are significantly different than before. So we pulled data on D30 media ROI for top gaming publishers.

With organic revenue included, it looks not too bad at first glance.

However, there’s a clear dip on Android and iOS at a very interesting time: right after Apple released iOS 14.5 and SKAdNetwork became a real, functioning, must-take-action thing. Right at the time, of course, when at least hundreds of millions of dollars of ad spend — and possibly billions — left the iOS ecosystem for Android.

For the Android side of the house, that’s further evidence that more dollars were chasing the same number of app installs, depressing organic installs as a percentage of all Android installs. On iOS, while ROI bounced back somewhat in May, April was a huge drop and May isn’t back up to the typical levels of January, February, and March.

Interestingly, when you take organic revenue out of the picture, iOS looks worse than Android for return on ad spend. There are a number of potential reasons for that, including a larger organic multiplier effect on iOS than Android and likely a few other factors … but that’s fodder for another day’s data dive.

Note: It’s important to not take the June ROI dip too seriously: since we’re looking at D30 ROI here, close to half the installs are not completely realizing their expected ROI yet and a big percentage is not even halfway there.

Summing up: change is the only constant

Hey: it’s 2021. It’s like 2020, only even crazier.

There’s a lot of change happening in the mobile marketing ecosystem, and not every player has caught up yet. In addition, it’s clear that mobile attribution as we once knew it is dead, and next-generation attribution is not just a nice-to-have anymore.

It’s essential.

There is no longer one way of generating accurate and reliable attribution truth on iOS. Instead, there are multiple datasets from a myriad of sources, some deterministic, some probabilistic, some bottom-funnel, and some top-funnel. All of this needs to be combined for the 20-30 different ad partners top-performing marketers are using.

And then next-gen attribution platforms also need to take into account web, offline, email, owned, and any other marketing modality that top marketers are using, whether paid, earned, or owned.

We are not in Kansas anymore.